Income tax rates describing the percentage at which individuals, corporate entities or other organizations are taxed, in Pakistan the Federal Board of Revenue (FBR) uses an unconventional tax rate system, in which the percentage of tax charged increases as the amount of the person's or entity's taxable income increases, a tax rate results in a higher rupee amount collected from taxpayers with greater incomes.

To help build and maintain the infrastructures used in a country, the government usually taxes its residents. The tax collected is used for the betterment of the nation, of society, and of all living in it. In Pakistan and many other countries around the world, a tax rate is applied to some form of money received by a taxpayer. The money could be income earned from salary, wages, investment income (dividends, interest), capital gains from investments, profits made from goods or services rendered, etc. The percentage of the taxpayer’s earnings or money is taken and remitted to the federal government.

When it comes to income tax, the tax rate is the percentage of an individual's taxable income or a

RIZWAN & ASSOCIATES - LLP | INCOME TAX RATES- PAKISTAN

corporate entity's earnings that is owed to federal government. The tax rate that is applied to an individual’s earnings depends on the marginal tax bracket that the individual falls under. The marginal tax rate is the percentage taken from the next rupee of taxable income above a pre-defined income limit.

TAX RATES | TAX YEAR 2022-2023

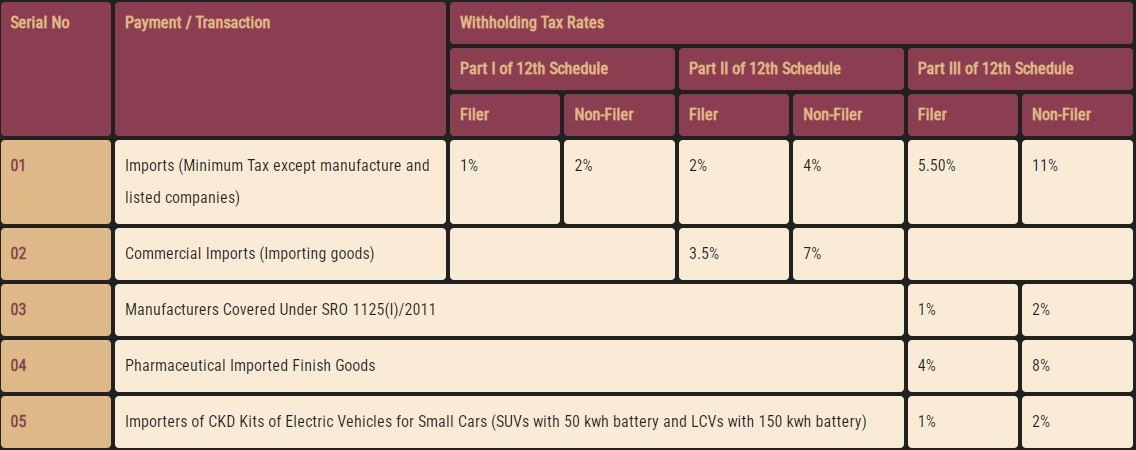

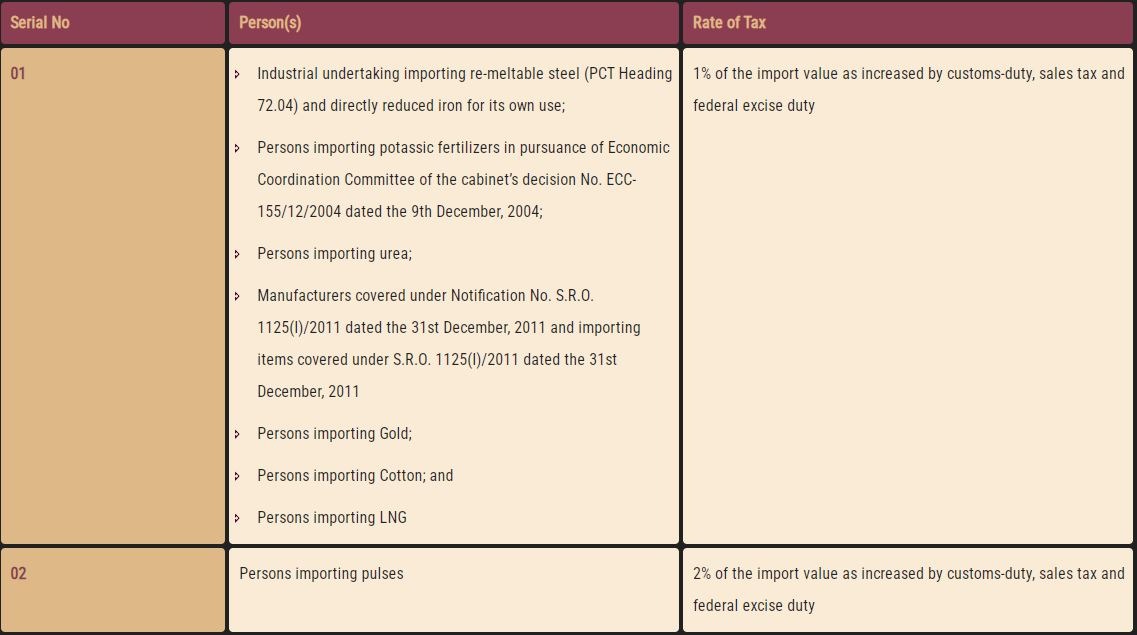

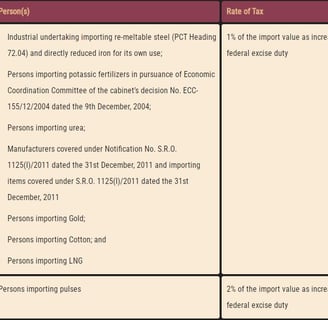

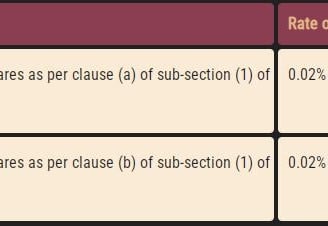

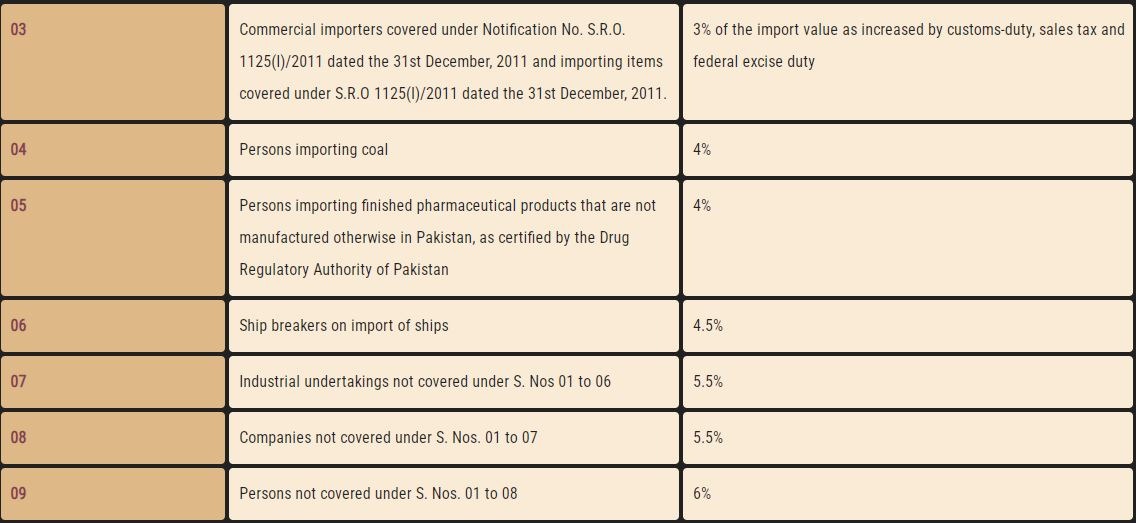

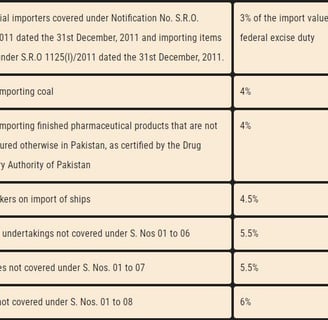

WITHHOLDING TAX RATES ON IMPORTS

Sec. 148, Part II, 1st Schedule | Part I-III, Twelfth Schedule

The rate of advance tax to be collected by the Collector of Customs:

Table: Tax on Petroleum Products

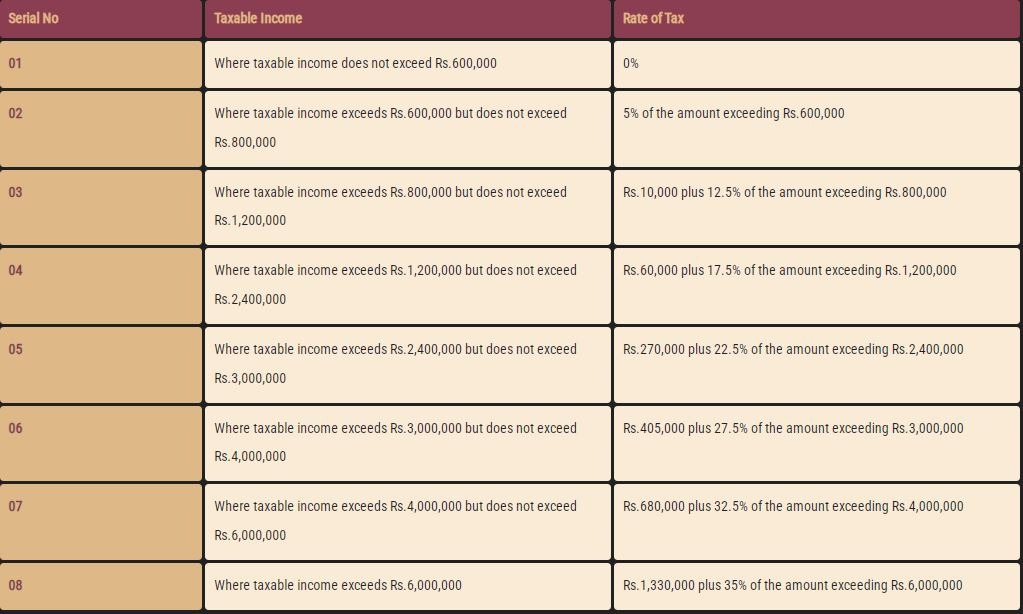

TAX RATES FOR SALARIED INDIVIDUALS

Sec. 149, Division I, Part I, 1st Schedule

Where the income of an individual chargeable under the head "salary" exceeds seventy-five percent of his taxable income, the following rates of tax will apply, which are unchanged from the previous tax year:

Table: Withholding Tax Rates on Imports

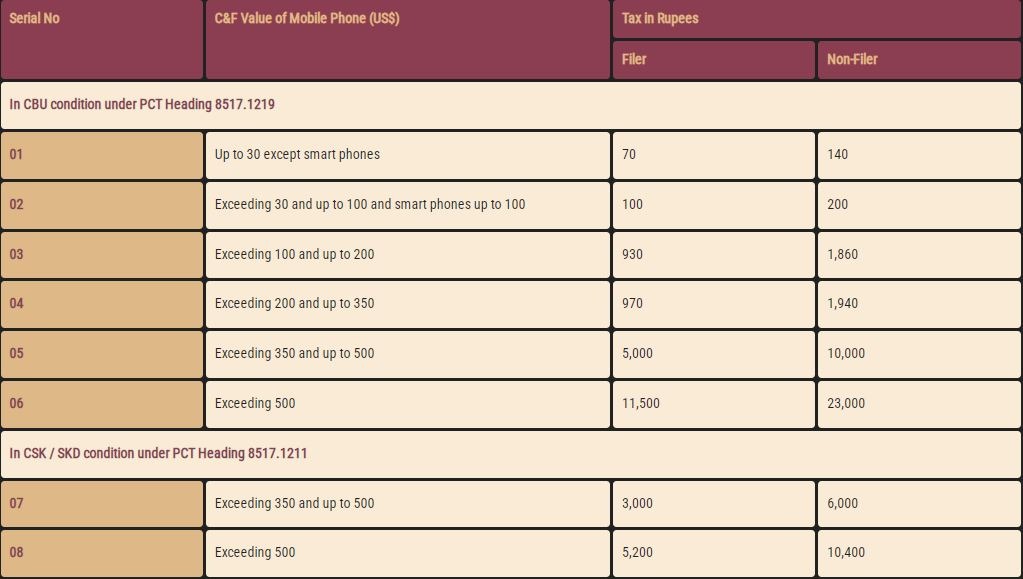

WITHHOLDING TAX ON IMPORT OF MOBILE PHONES

Sec. 148

Table: Tax Rates for Salaried Individuals

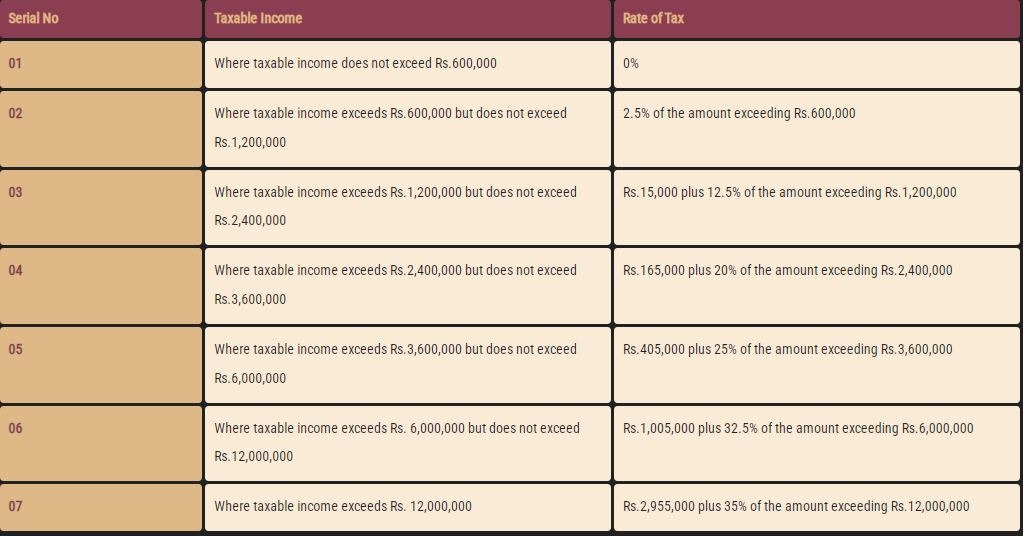

TAX RATES FOR INDIVIDUALS & ASSOCIATION OF PERSONS

Division I, Part I, 1st Schedule

No change in the tax rates for individuals and association of persons has been made. the tax rates applicable for the Tax Year 2022 are set out in the following table:

Table: Tax Rates for Individuals & Association of Persons

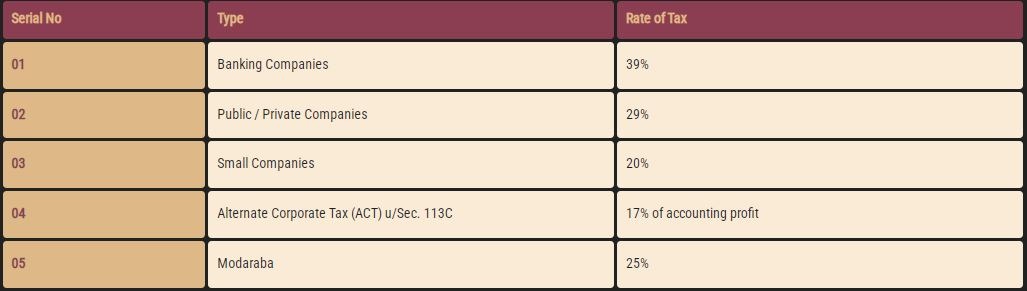

TAX RATES FOR COMPANIES

Division II, Part I, 1st Schedule

Tax rates for a banking company, public & private company, small company, alternate corporate tax and modaraba are given in the following table:

Table: Tax Rates for Companies | Where the taxpayer is a small company , tax shall be payable at the rate of 20% for the Tax Year 2023 and onward.

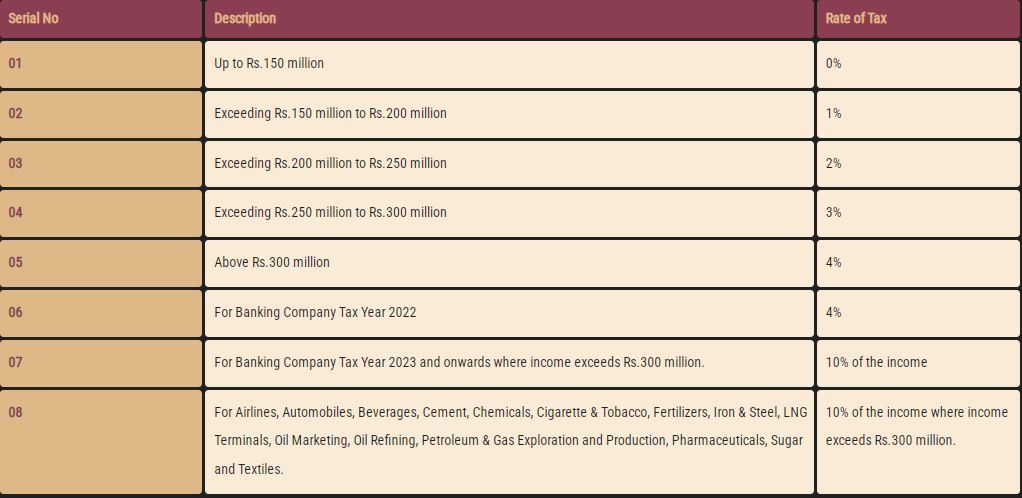

SUPER TAX

Rate of Super Tax on high earning persons (Sec. 4C)

Table: Super Tax

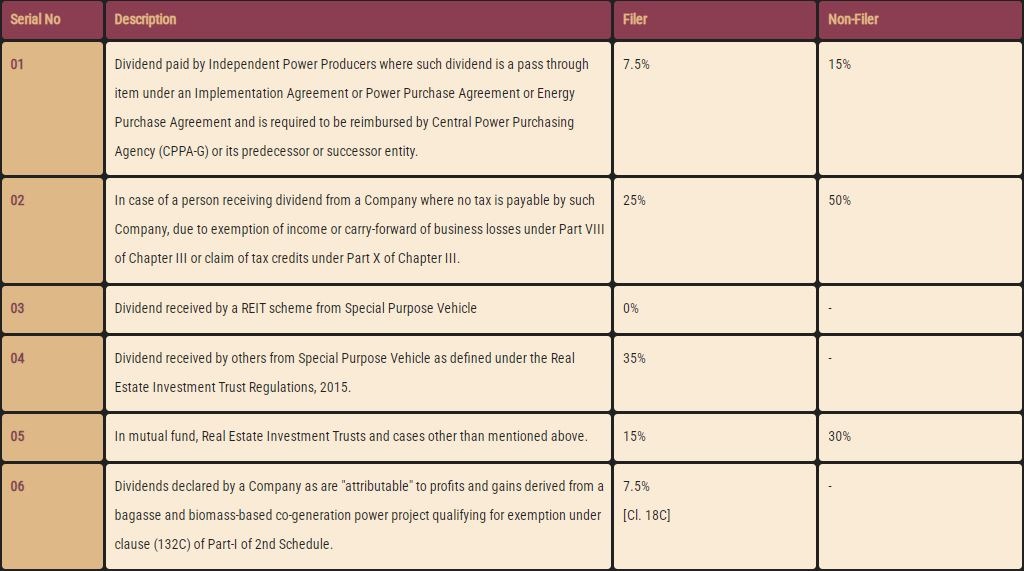

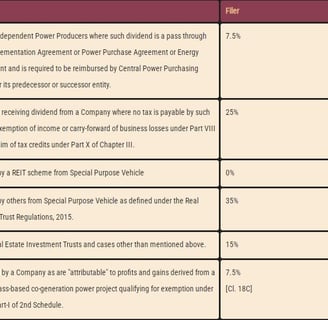

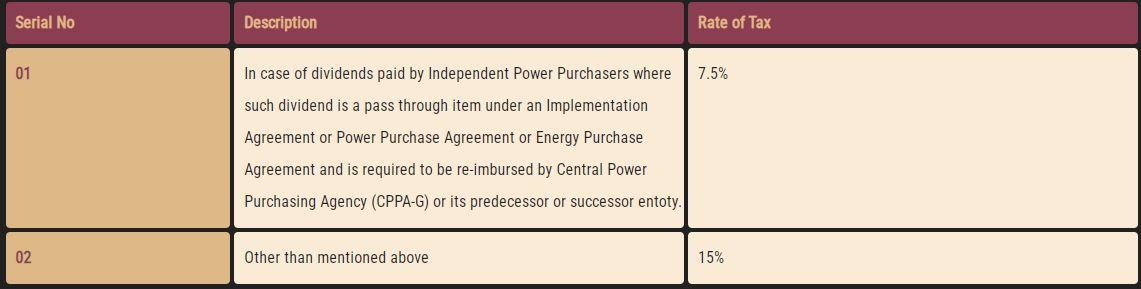

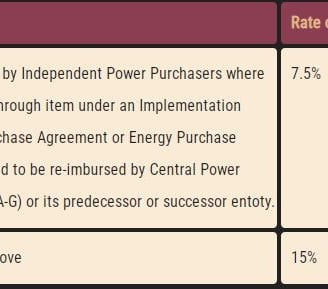

DIVIDEND TAX

Sec. 150

Person paying a dividend shall deduct tax from the gross amount of the dividend paid or collect tax from the amount of dividend in specie.

Table: Dividend Tax

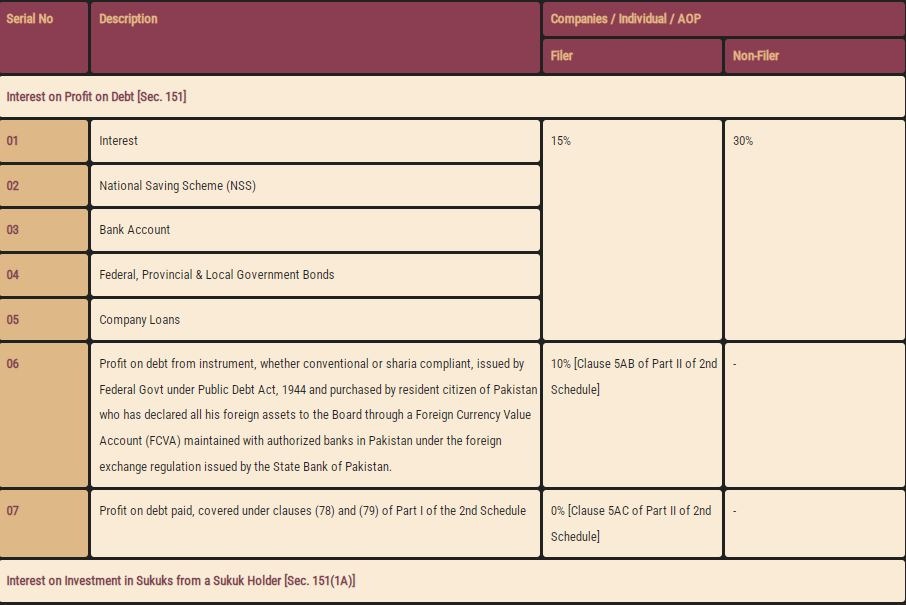

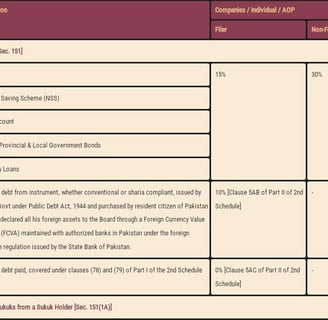

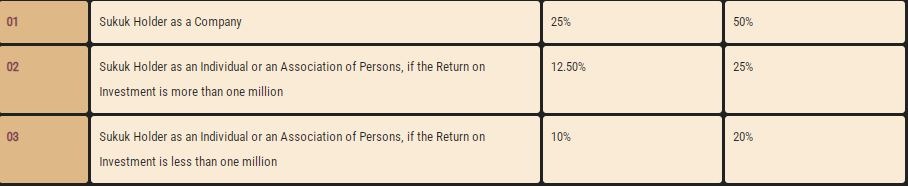

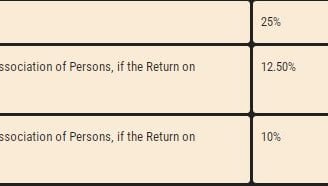

TAX ON PROFIT ON DEBT & RETURN ON INVESTMENT IN SUKUKS

Sec. 151, Division 1A & 1B, Part III, 1st Schedule

Table: Tax on Profit on Debt & Return on Investment in Sukuks

TAX ON NON-RESIDENTS

Sec 152, Division IV, Part I, 1st Schedule

Table: Tax on Non-Residents

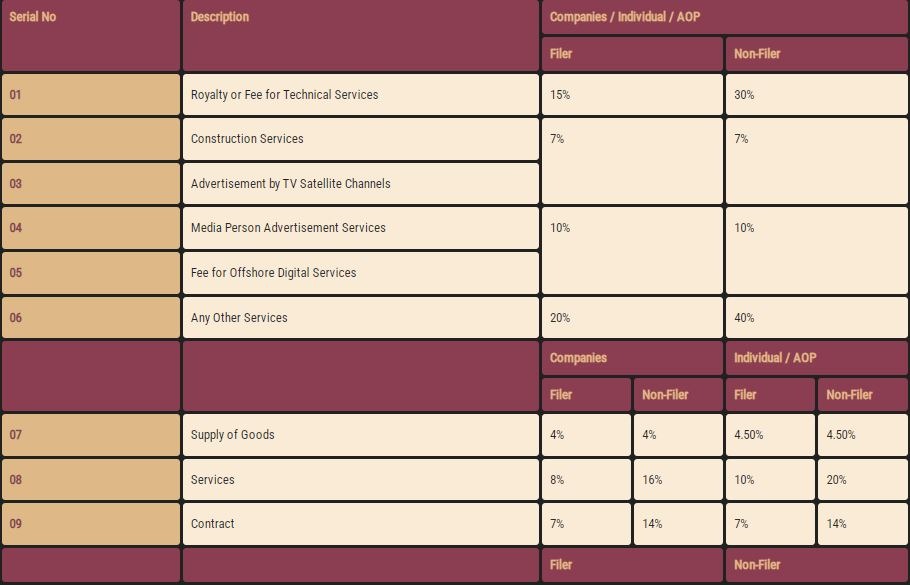

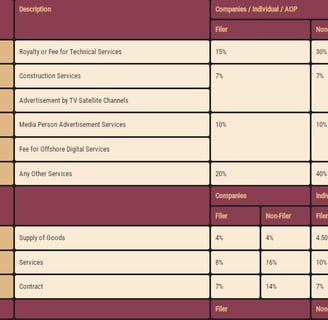

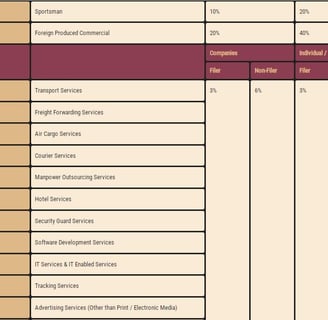

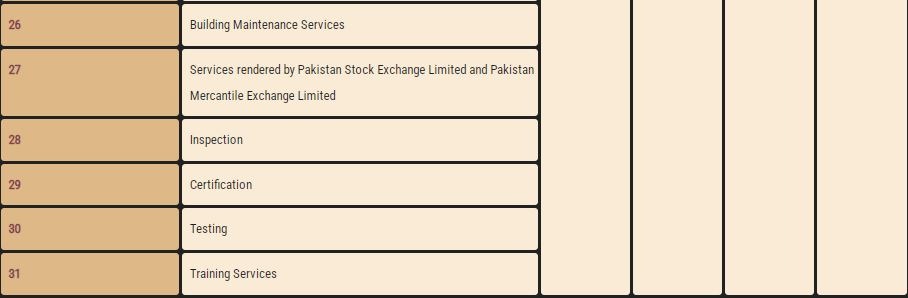

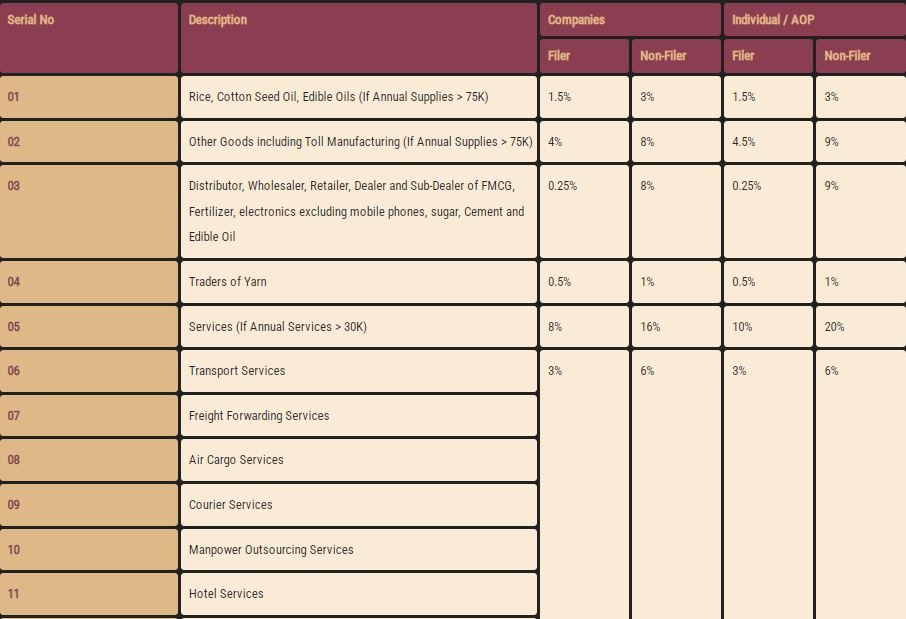

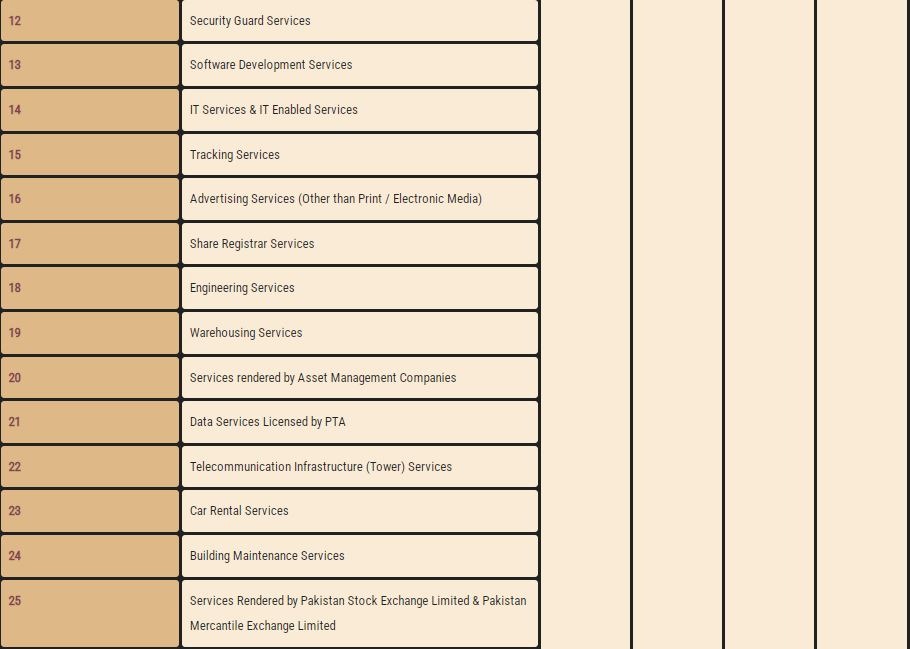

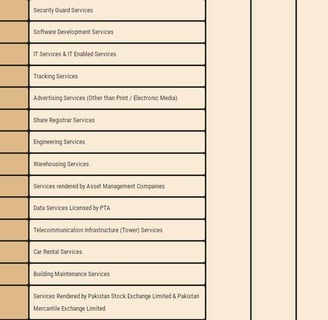

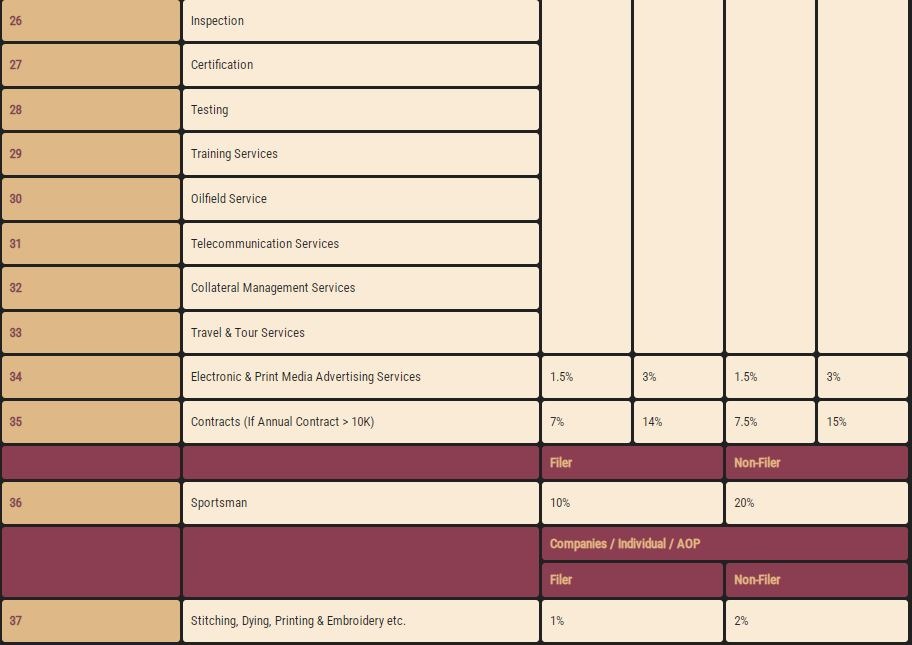

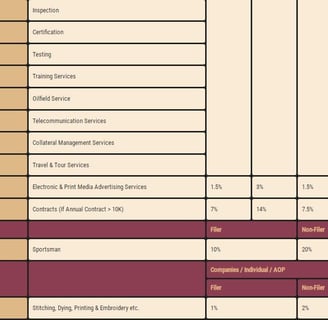

TAX ON GOODS, SERVICES & CONTRACTS

Sec. 153, Division III A, Part III, 1st Schedule

Table: Tax on Profit on Debt & Return on Investment in Sukuks

TAX ON NON-RESIDENTS

Sec 152, Division IV, Part I, 1st Schedule

Table: Tax on Goods, Services & Contracts

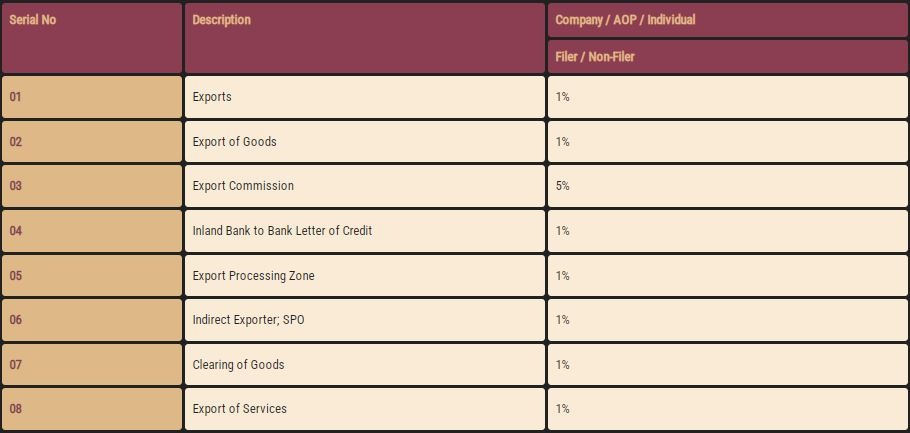

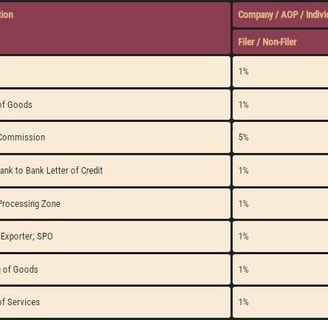

TAX RATES ON EXPORTS & EXPORT OF SERVICES

Sec. 154 & 154A, Division IV, Part III, 1st Schedule

Table: Tax Rates on Exports & Export of Services

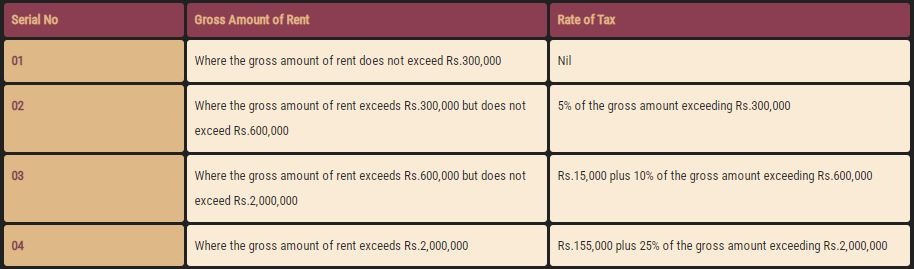

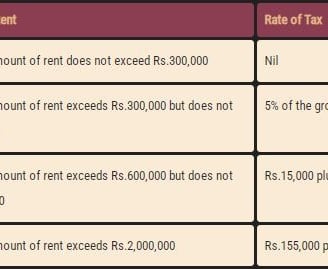

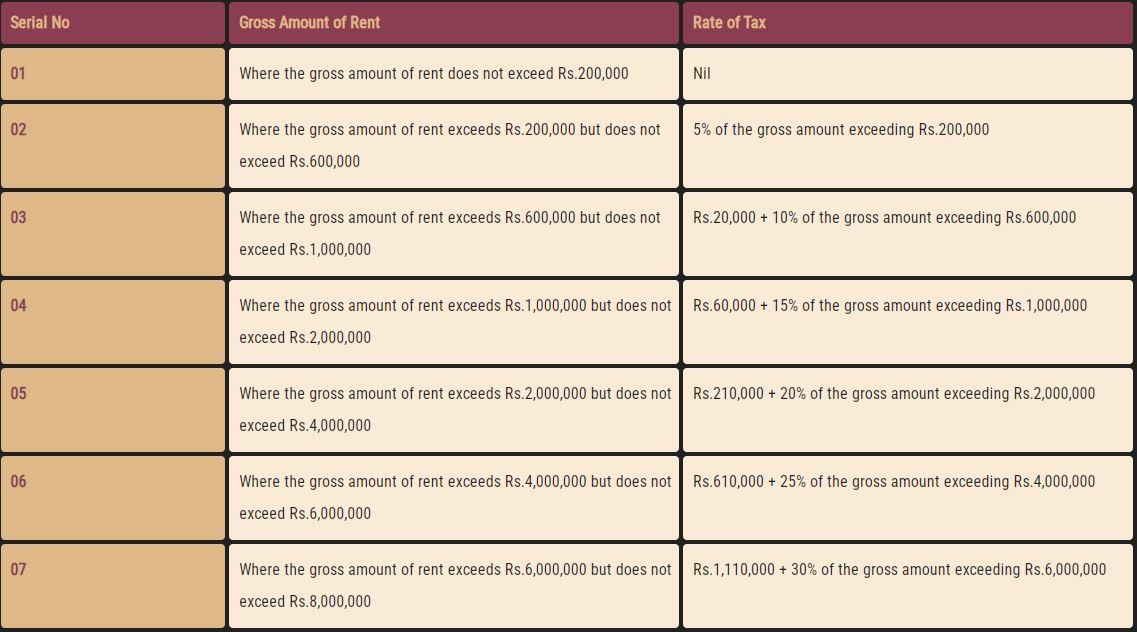

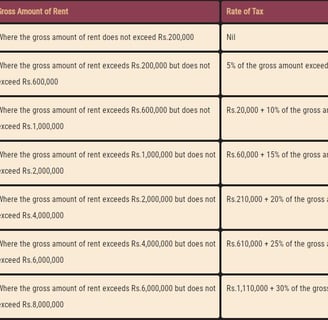

TAX ON RENT OF IMMOVABLE PROPERTY

Sec. 155, Division V, Part III, 1st Schedule

Table: Tax on Rent of Immovable Property | The rate of tax to be deducted u/Sec. 155, in case of company shall be 15% of the gross amount of rent.

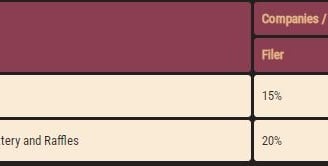

TAX ON PRIZES & WINNINGS

Sec. 156, Division VI, Part III, 1st Schedule

Table: Tax on Prizes & Winnings

TAX ON PETROLEUM PRODUCTS

Sec. 156A, Division VIA, Part III, 1st Schedule

Table: Tax on Petroleum Products

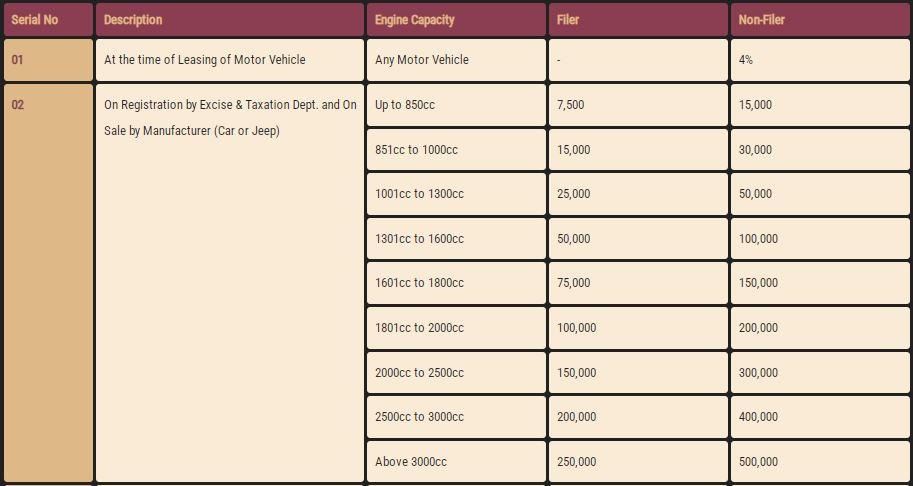

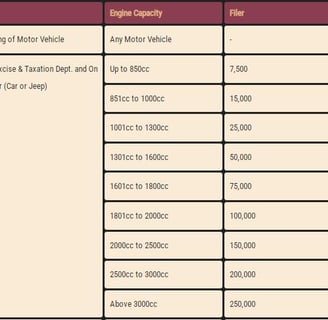

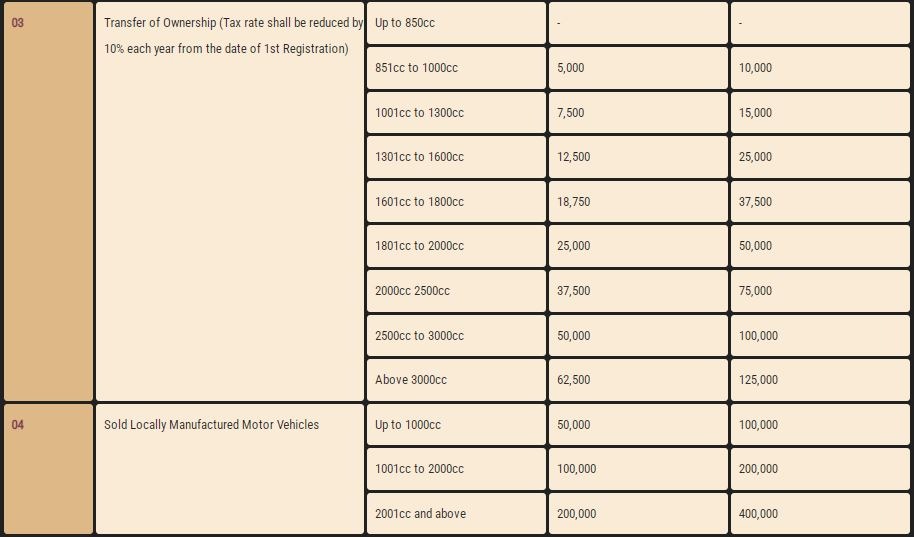

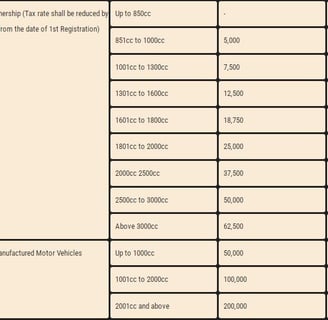

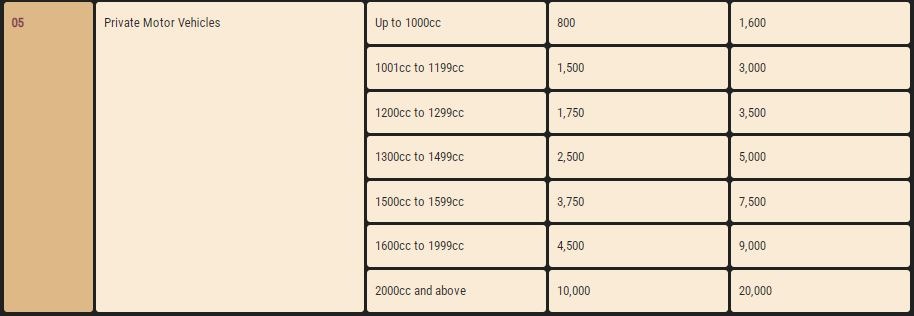

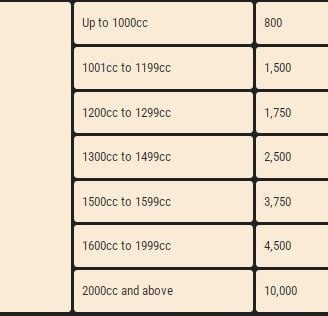

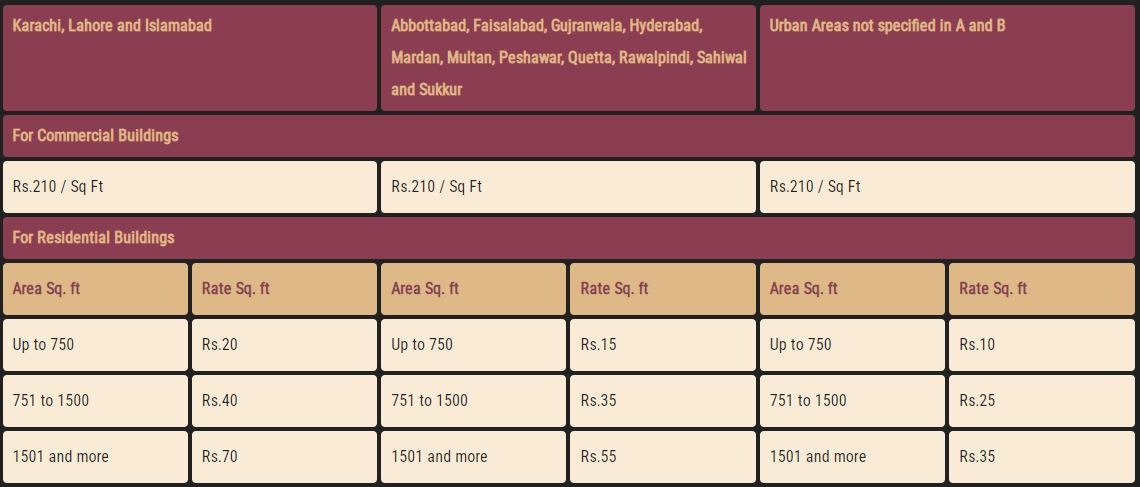

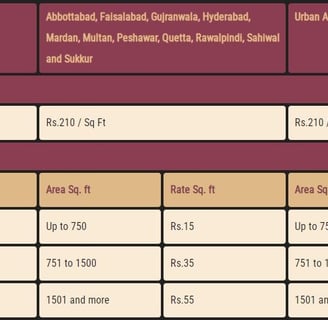

ADVANCE TAX ON PURCHASE, REGISTRATION AND TRANSFER OF MOTOR VEHICLES

Sec. 231B & 234, Division VII, Part IV, 1st Schedule

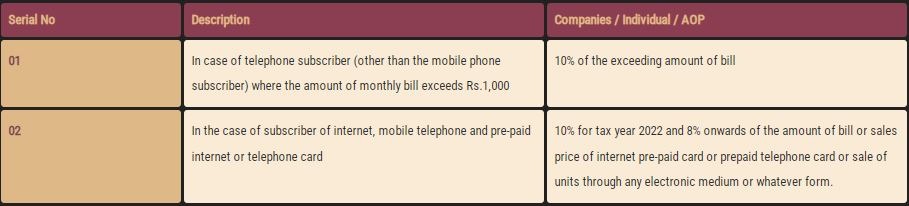

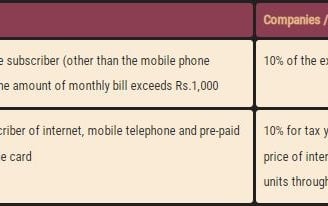

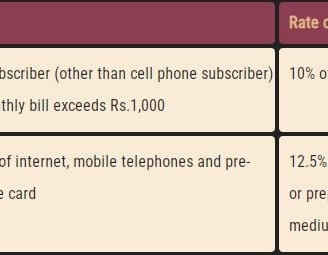

Table: Tax on Telephone and Internet

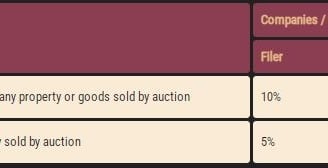

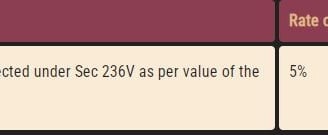

ADVANCE TAX AT THE TIME OF SALE BY AUCTION

Sec. 236A, Division VIII, Part IV, 1st Schedule

Table: Advance Tax on Purchase, Registration & Transfer

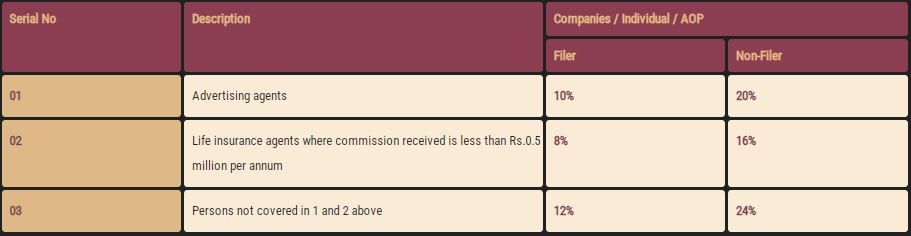

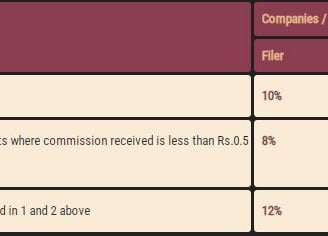

TAX ON BROKERAGE AND COMMISSION

Sec. 233, Division II, Part IV, 1st Schedule

Table: Tax on Brokerage and Commission

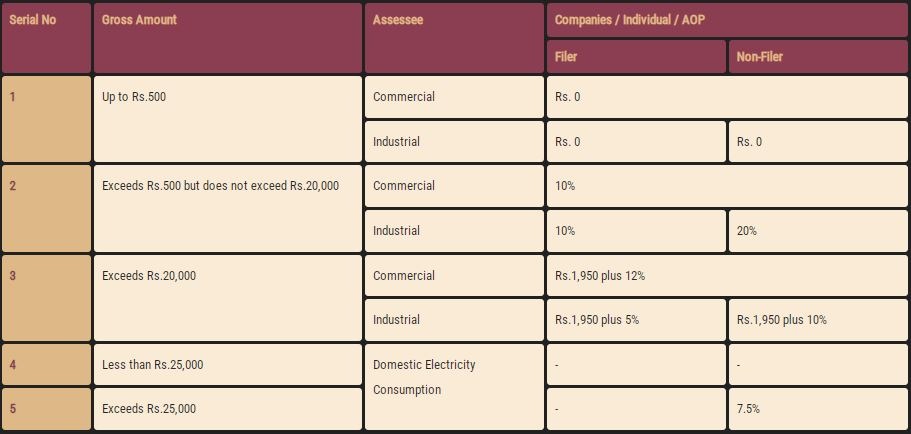

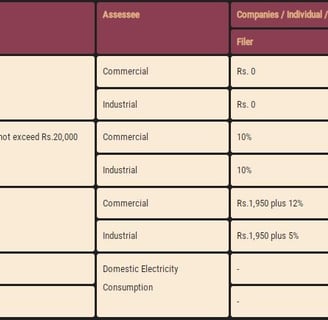

TAX ON ELECTRICITY CONSUMPTION

Sec. 235, Division IV, Part IV, 1st Schedule

Table: Tax on Electricity Consumption

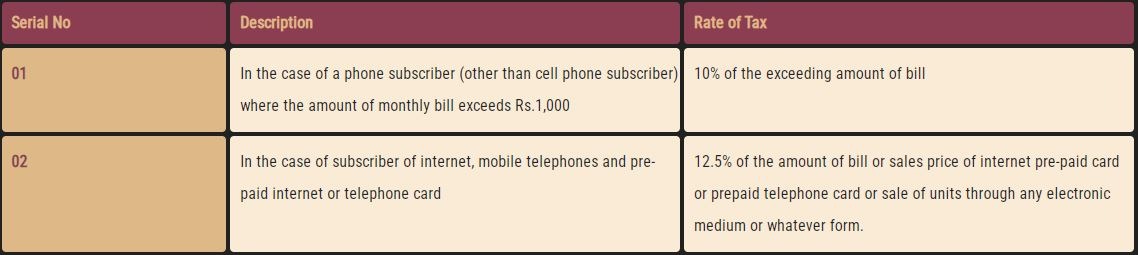

TAX ON TELEPHONE AND INTERNET

Sec. 236, Division IV, Part IV, 1st Schedule

Table: Advance Tax at the time of sale by auction

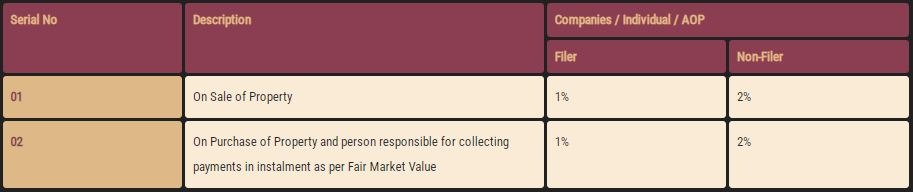

ADVANCE TAX ON SALE & PURCHASE OF IMMOVABLE PROPERTY

Sec. 236C & 236K, Division X & XVIII, Part IV, 1st Schedule

Table: Advance Tax on Sale & Purchase of Immovable Property

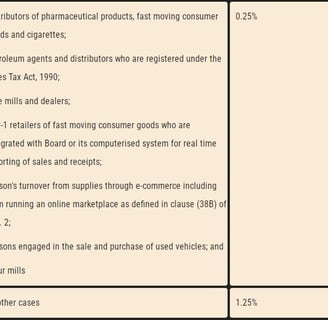

ADVANCE TAX ON DISTRIBUTORS, DEALERS OR WHOLESALERS

Sec. 236G, Division XIV, Part IV, 1st Schedule

Table: Advance Tax on Distributors, Dealers or Wholesalers

ADVANCE TAX ON SALE TO RETAILERS

Sec. 236H, Division XV, Part IV, 1st Schedule

Table: Advance Tax on Sale to Retailers

COLLECTION OF ADVANCE TAX BY EDUCATIONAL INSTITUTIONS

Sec. 236I, Division XVI, Part IV, 1st Schedule

Table: Collection of Advance Tax by Educational Institutions

PAYMENT TO A RESIDENT PERSON FOR RIGHT TO USE MACHINERY & EQUIPMENT

Sec. 236Q, Division XXIII, Part IV, 1st Schedule

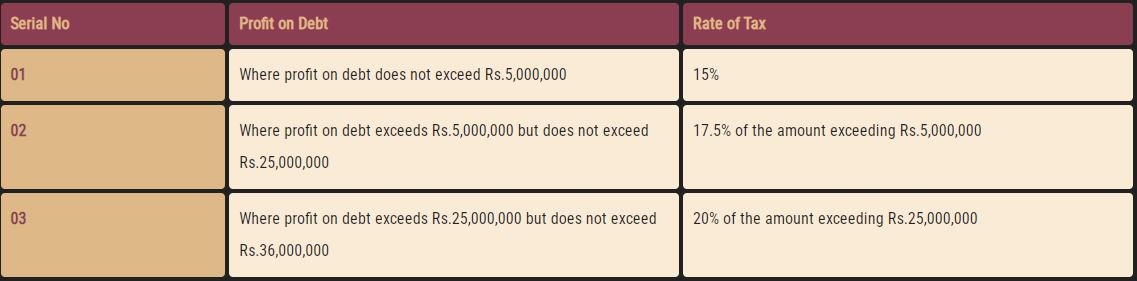

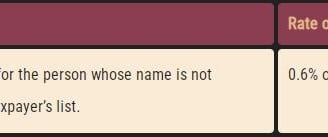

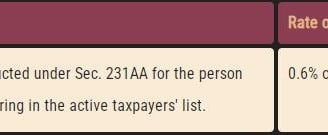

Table: Tax for Profit on Debt | As per 10th Schedule, Tax Rate shall be increased by 100% in case the person is not appearing in Active Taxpayers' List.

Profit on Debt exceeding Rs.36 million shall be subject to tax under normal law.

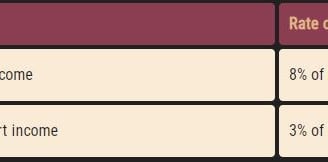

TAX ON SHIPPING OR AIR TRANSPORT INCOME OF A NON-RESIDENT PERSON

Table: Tax on Shipping or Air Transport Income

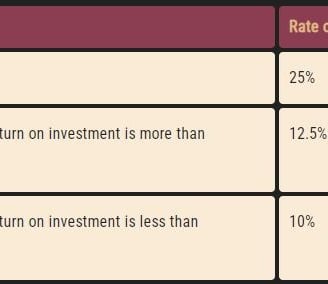

TAX ON RETURN ON INVESTMENT IN SUKUKS

Sec. 5AA, Division IB, Part III, 1st Schedule

Table: Payment to Resident Person in using Machinery & Equipment

TAX FOR PROFIT ON DEBT - OTHER THAN A COMPANY

Sec. 7B, Division III A, Part I, 1st Schedule

Table: Tax on Return on Investment | As per 10th Schedule, Tax Rate shall be increased by 100% in case the person is not appearing in Active Taxpayers' List

TAX ON CERTAIN PAYMENTS TO NON-RESIDENTS

Table: Tax on Certain Payments to Non-Residents | As per 10th Schedule, Tax Rate shall be increased by 100% in case the person is not appearing in Active Taxpayers' List

TAX ON INCOME FROM PROPERTY FOR INDIVIDUALS AND ASSOCIATION OF PERSONS

Sec. 15, Division V, Part I, 1st Schedule

Table: Tax on Income from Property

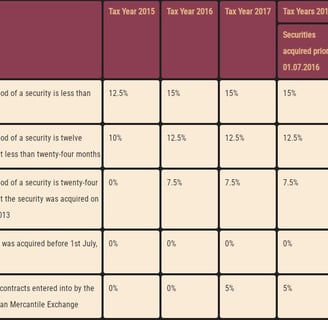

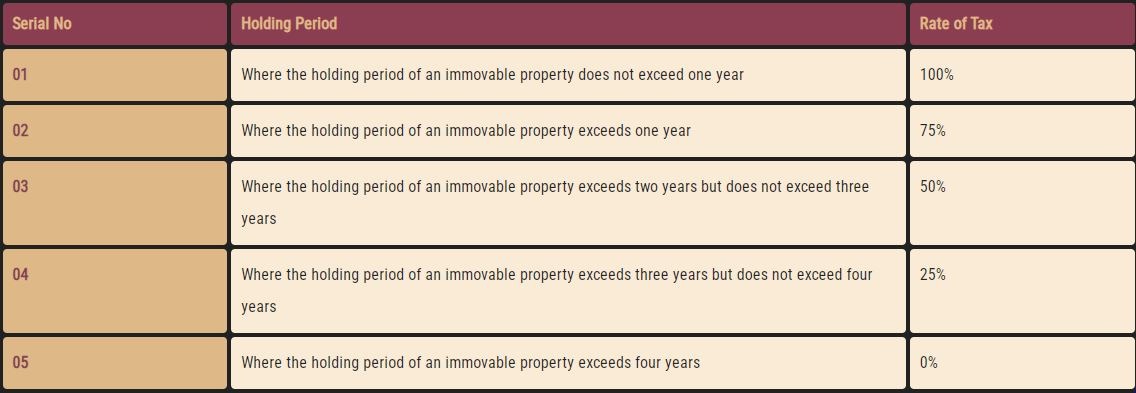

CAPITAL GAINS ON DISPOSAL OF SECURITIES

Sec. 37A, Division VII, Part I, 1st Schedule

Table: Capital Gains on Disposal of Securities | The rate of tax on cash settled derivatives traded on the stock exchange shall be 5% for the tax years 2018 to 2020.

A Mutual Fund or a Collective Investment Scheme or a REIT Scheme shall deduct Capital Gains Tax at the rates as specified below on Redemption of Securities, as specified below:

Provided further that in case of a stock fund if dividend receipts of the fund are less than capital gains, then the rate of tax deduction shall be 12.5%. No capital gains tax shall be deducted, if the holding period of the security is more than 4 years.

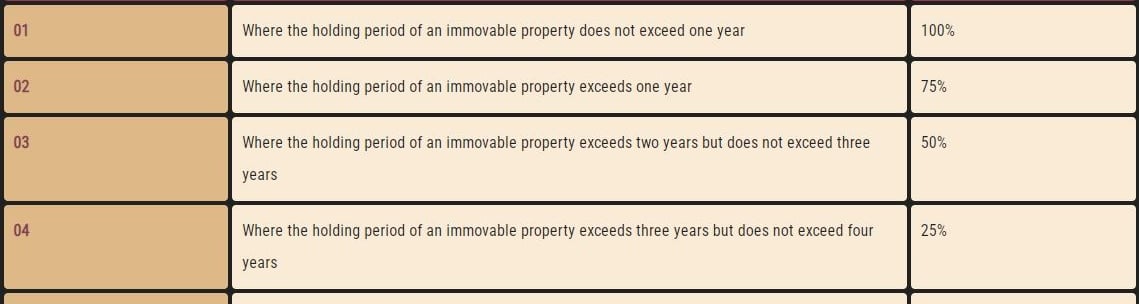

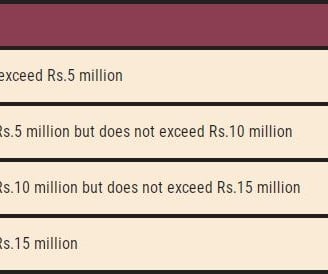

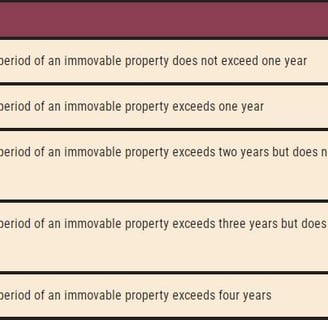

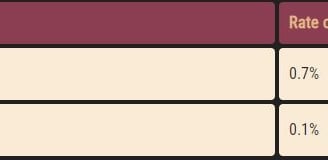

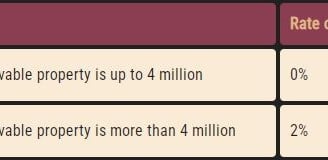

CAPITAL GAINS ON DISPOSAL OF IMMOVABLE PROPERTY (CAPITAL ASSETS)

Sec. 37(1A), Division VIII, Part I, 1st Schedule

Table: Capital Gains on Disposal of Immovable Property

CAPITAL GAINS ON DISPOSAL OF IMMOVABLE PROPERTY

Sec. 37(3A)

TAX RATES | TAX YEAR 2022-2023

WITHHOLDING TAX RATES ON IMPORTS

Sec. 148, Part II, 1st Schedule | Part I-III, Twelfth Schedule

The rate of advance tax to be collected by the Collector of Customs:

Table: Tax on Petroleum Products

TAX RATES FOR SALARIED INDIVIDUALS

Sec. 149, Division I, Part I, 1st Schedule

Where the income of an individual chargeable under the head "salary" exceeds seventy-five percent of his taxable income, the following rates of tax will apply, which are unchanged from the previous tax year:

Table: Withholding Tax Rates on Imports

WITHHOLDING TAX ON IMPORT OF MOBILE PHONES

Sec. 148

Table: Tax Rates for Salaried Individuals

TAX RATES FOR INDIVIDUALS & ASSOCIATION OF PERSONS

Division I, Part I, 1st Schedule

No change in the tax rates for individuals and association of persons has been made. the tax rates applicable for the Tax Year 2022 are set out in the following table:

Table: Tax Rates for Individuals & Association of Persons

TAX RATES FOR COMPANIES

Division II, Part I, 1st Schedule

Tax rates for a banking company, public & private company, small company, alternate corporate tax and modaraba are given in the following table:

Table: Tax Rates for Companies | Where the taxpayer is a small company , tax shall be payable at the rate of 20% for the Tax Year 2023 and onward.

SUPER TAX

Rate of Super Tax on high earning persons (Sec. 4C)

Table: Super Tax

DIVIDEND TAX

Sec. 150

Person paying a dividend shall deduct tax from the gross amount of the dividend paid or collect tax from the amount of dividend in specie.

Table: Dividend Tax

TAX ON PROFIT ON DEBT & RETURN ON INVESTMENT IN SUKUKS

Sec. 151, Division 1A & 1B, Part III, 1st Schedule

Table: Tax on Profit on Debt & Return on Investment in Sukuks

TAX ON NON-RESIDENTS

Sec 152, Division IV, Part I, 1st Schedule

Table: Tax on Non-Residents

TAX ON GOODS, SERVICES & CONTRACTS

Sec. 153, Division III A, Part III, 1st Schedule

Table: Tax on Profit on Debt & Return on Investment in Sukuks

TAX ON NON-RESIDENTS

Sec 152, Division IV, Part I, 1st Schedule

Table: Tax on Goods, Services & Contracts

TAX RATES ON EXPORTS & EXPORT OF SERVICES

Sec. 154 & 154A, Division IV, Part III, 1st Schedule

Table: Tax Rates on Exports & Export of Services

TAX ON RENT OF IMMOVABLE PROPERTY

Sec. 155, Division V, Part III, 1st Schedule

Table: Tax on Rent of Immovable Property | The rate of tax to be deducted u/Sec. 155, in case of company shall be 15% of the gross amount of rent.

TAX ON PRIZES & WINNINGS

Sec. 156, Division VI, Part III, 1st Schedule

Table: Tax on Prizes & Winnings

TAX ON PETROLEUM PRODUCTS

Sec. 156A, Division VIA, Part III, 1st Schedule

Table: Tax on Petroleum Products

ADVANCE TAX ON PURCHASE, REGISTRATION AND TRANSFER OF MOTOR VEHICLES

Sec. 231B & 234, Division VII, Part IV, 1st Schedule

Table: Tax on Telephone and Internet

ADVANCE TAX AT THE TIME OF SALE BY AUCTION

Sec. 236A, Division VIII, Part IV, 1st Schedule

Table: Advance Tax on Purchase, Registration & Transfer

TAX ON BROKERAGE AND COMMISSION

Sec. 233, Division II, Part IV, 1st Schedule

Table: Tax on Brokerage and Commission

TAX ON ELECTRICITY CONSUMPTION

Sec. 235, Division IV, Part IV, 1st Schedule

Table: Tax on Electricity Consumption

TAX ON TELEPHONE AND INTERNET

Sec. 236, Division IV, Part IV, 1st Schedule

Table: Advance Tax at the time of sale by auction

ADVANCE TAX ON SALE & PURCHASE OF IMMOVABLE PROPERTY

Sec. 236C & 236K, Division X & XVIII, Part IV, 1st Schedule

Table: Advance Tax on Sale & Purchase of Immovable Property

ADVANCE TAX ON DISTRIBUTORS, DEALERS OR WHOLESALERS

Sec. 236G, Division XIV, Part IV, 1st Schedule

Table: Advance Tax on Distributors, Dealers or Wholesalers

ADVANCE TAX ON SALE TO RETAILERS

Sec. 236H, Division XV, Part IV, 1st Schedule

Table: Advance Tax on Sale to Retailers

COLLECTION OF ADVANCE TAX BY EDUCATIONAL INSTITUTIONS

Sec. 236I, Division XVI, Part IV, 1st Schedule

Table: Collection of Advance Tax by Educational Institutions

PAYMENT TO A RESIDENT PERSON FOR RIGHT TO USE MACHINERY & EQUIPMENT

Sec. 236Q, Division XXIII, Part IV, 1st Schedule

Table: Tax for Profit on Debt | As per 10th Schedule, Tax Rate shall be increased by 100% in case the person is not appearing in Active Taxpayers' List.

Profit on Debt exceeding Rs.36 million shall be subject to tax under normal law.

TAX ON SHIPPING OR AIR TRANSPORT INCOME OF A NON-RESIDENT PERSON

Table: Tax on Shipping or Air Transport Income

TAX ON RETURN ON INVESTMENT IN SUKUKS

Sec. 5AA, Division IB, Part III, 1st Schedule

Table: Payment to Resident Person in using Machinery & Equipment

TAX FOR PROFIT ON DEBT - OTHER THAN A COMPANY

Sec. 7B, Division III A, Part I, 1st Schedule

Table: Tax on Return on Investment | As per 10th Schedule, Tax Rate shall be increased by 100% in case the person is not appearing in Active Taxpayers' List

TAX ON CERTAIN PAYMENTS TO NON-RESIDENTS

Table: Tax on Certain Payments to Non-Residents | As per 10th Schedule, Tax Rate shall be increased by 100% in case the person is not appearing in Active Taxpayers' List

TAX ON INCOME FROM PROPERTY FOR INDIVIDUALS AND ASSOCIATION OF PERSONS

Sec. 15, Division V, Part I, 1st Schedule

Table: Tax on Income from Property

CAPITAL GAINS ON DISPOSAL OF SECURITIES

Sec. 37A, Division VII, Part I, 1st Schedule

Table: Capital Gains on Disposal of Securities | The rate of tax on cash settled derivatives traded on the stock exchange shall be 5% for the tax years 2018 to 2020.

A Mutual Fund or a Collective Investment Scheme or a REIT Scheme shall deduct Capital Gains Tax at the rates as specified below on Redemption of Securities, as specified below:

Provided further that in case of a stock fund if dividend receipts of the fund are less than capital gains, then the rate of tax deduction shall be 12.5%. No capital gains tax shall be deducted, if the holding period of the security is more than 4 years.

CAPITAL GAINS ON DISPOSAL OF IMMOVABLE PROPERTY (CAPITAL ASSETS)

Sec. 37(1A), Division VIII, Part I, 1st Schedule

Table: Capital Gains on Disposal of Immovable Property

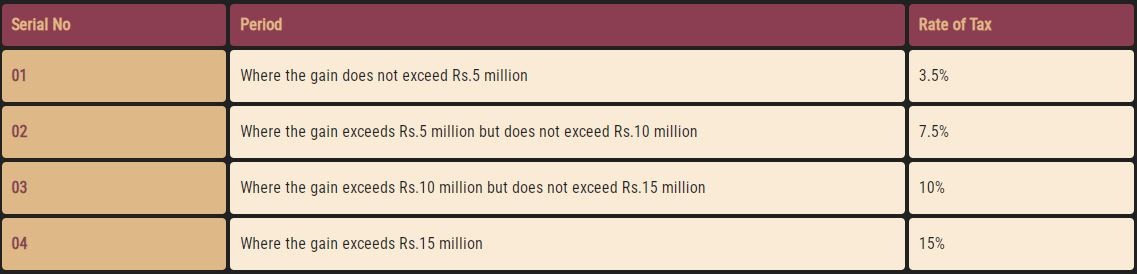

CAPITAL GAINS ON DISPOSAL OF IMMOVABLE PROPERTY

Sec. 37(3A)

Table: Capital Gains on Disposal of Immovable Property

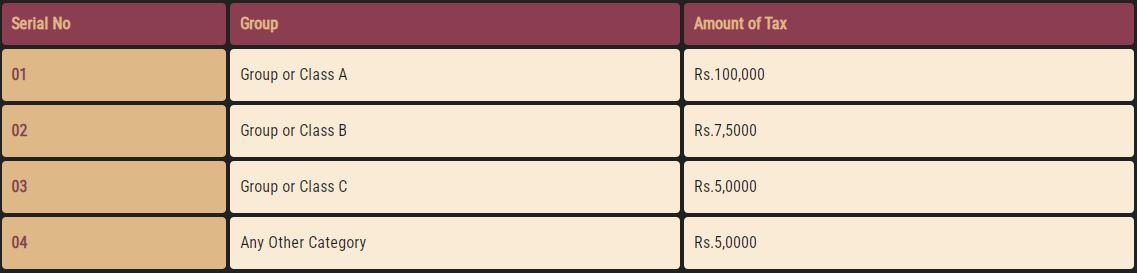

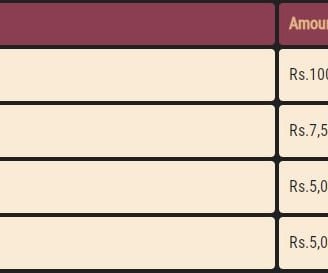

TAX ON BUILDERS

Sec. 7C, Division VIII A, Part I, 1st Schedule

Table: Capital Gains on Disposal of Immovable Property

TAX ON BUILDERS

Sec. 7C, Division VIII A, Part I, 1st Schedule

Table: Tax on Builders

TAX ON DEVELOPERS

Sec. 7D, Division VIII B, Part I, 1st Schedule

Table: Tax on Developers

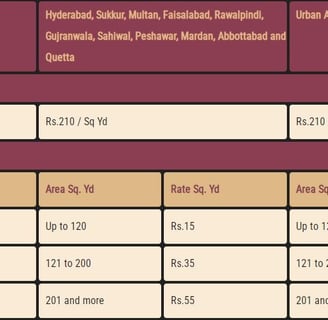

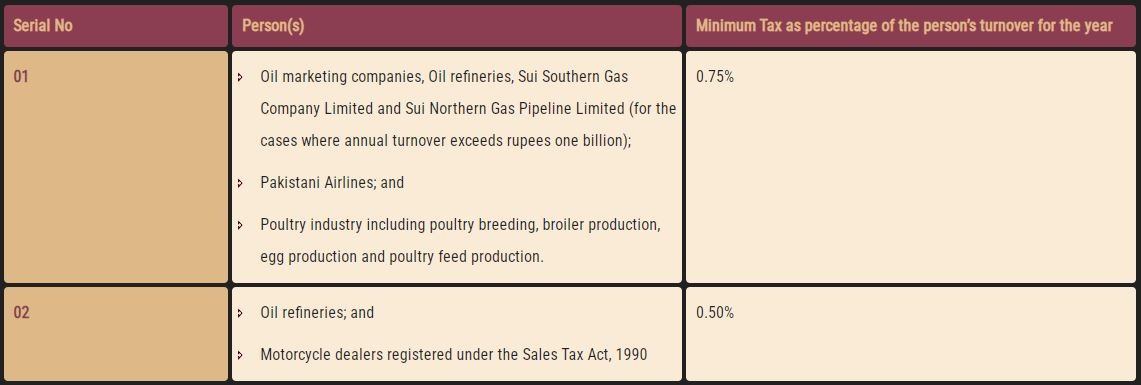

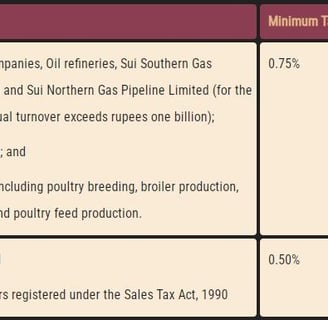

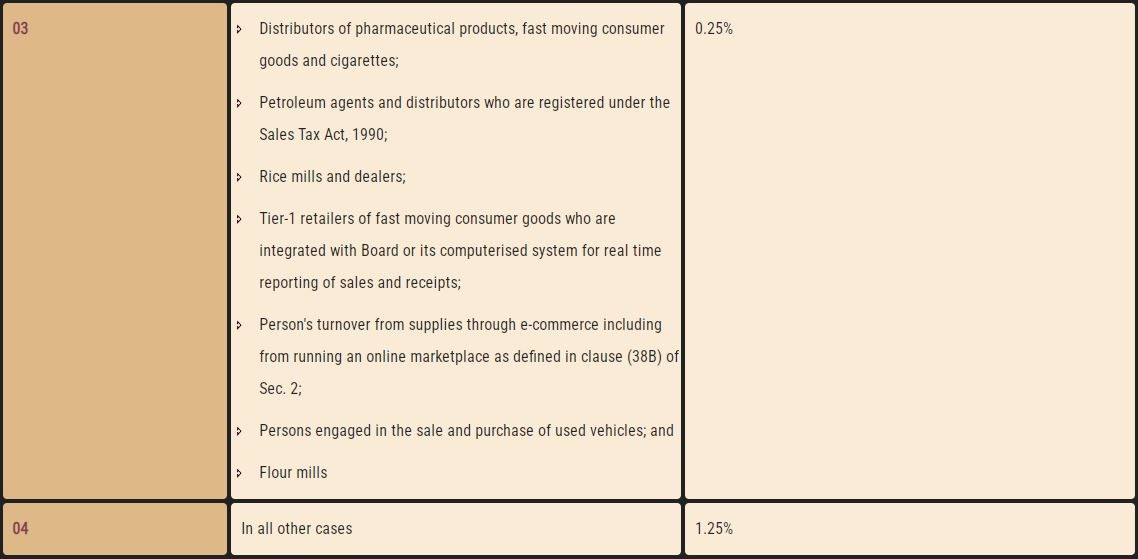

MINIMUM TAX

Sec. 113, Division IX, Part I, 1st Schedule

Table: Minimum Tax

REDUCTION IN TAX LIABILITY FOR FULL TIME TEACHER

Clause (2), Part III of 2nd Schedule

Table: Payment of Advance Tax

ADVANCE TAX

Table: Reduction in Tax Liability for Full Time Teacher

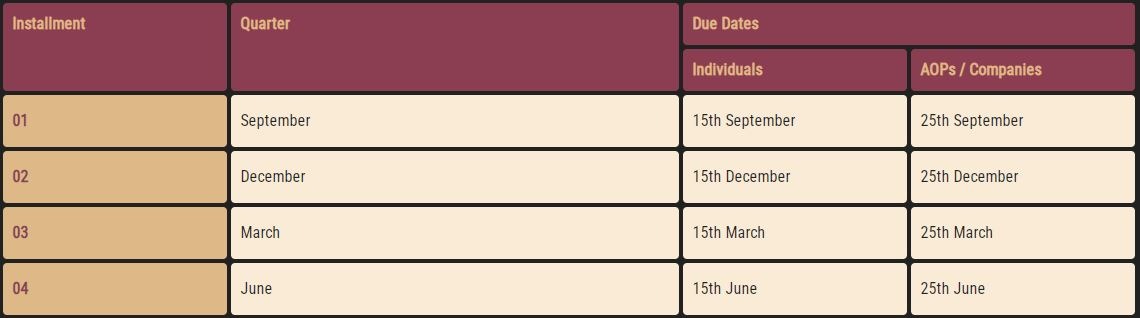

PAYMENT OF ADVANCE TAX

Sec. 147

Table: Advance Tax

ADVANCE TAX ON DIVIDEND

Table: Advance Tax on Dividend

COLLECTION OF TAX BY A REGISTERED STOCK EXCHANGE IN PAKISTAN

Table: Collection of Tax by a Stock Exchange in Pakistan

COLLECTION OF TAX ON PASSENGER TRANSPORT VEHICLES

Table: Collection of Tax on Passenger Transport Vehicles

COLLECTION OF TAX ON TELEPHONE USERS

Table: Collection of Tax on Telephone Users

TAX ON CASH WITHDRAWAL FROM A BANK

Table: Tax on Cash Withdrawal from a Bank

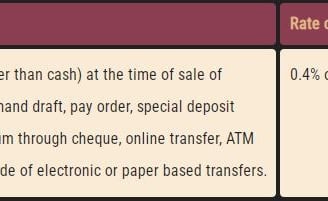

ADVANCE TAX ON TRANSACTIONS IN BANK [TRANSFEROR]

Table: Advance Tax on Transactions in Bank

ADVANCE TAX ON BANKING TRANSACTIONS OTHERWISE THAN THROUGH CASH [RECEIVER]

Table: Advance Tax on Banking Transactions Otherwise Than Through Cash

TAX ON CABLE TELEVISION OPERATOR

Table: Tax on Cable Television Operator

ADVANCE TAX ON SALE TO DISTRIBUTORS, DEALERS OR WHOLESALERS

Table: Advance Tax on Sale to Distributors, Dealers or Wholesalers

ADVANCE TAX ON DEALERS, COMMISSION AGENTS AND ARHATIS, ETC.

Table: Advance Tax on Dealers, Commission Agents and Arhatis, etc.

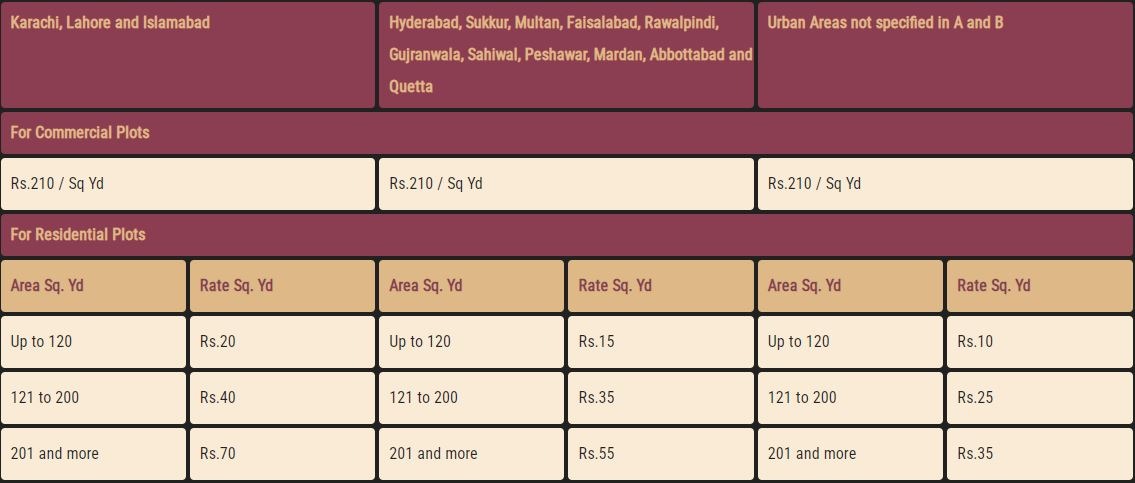

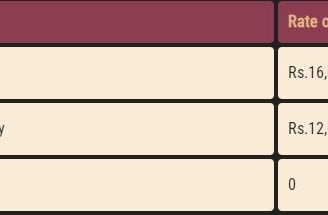

ADVANCE TAX ON PURCHASE OF IMMOVABLE PROPERTY

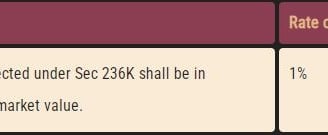

Table: Advance Tax on Purchase of Immovable Property | The rate of tax to be collected under Sec. 236K shall be 1% of the fair market value.

ADVANCE TAX ON SALE OR TRANSFER OF IMMOVABLE PROPERTY

Table: Advance Tax on Sale or Transfer of Immovable Property

ADVANCE TAX ON INTERNATIONAL AIR TICKET

Table: Advance Tax on International Air Ticket

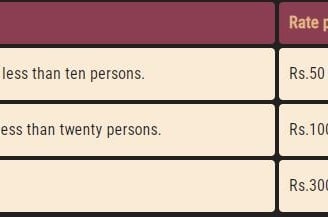

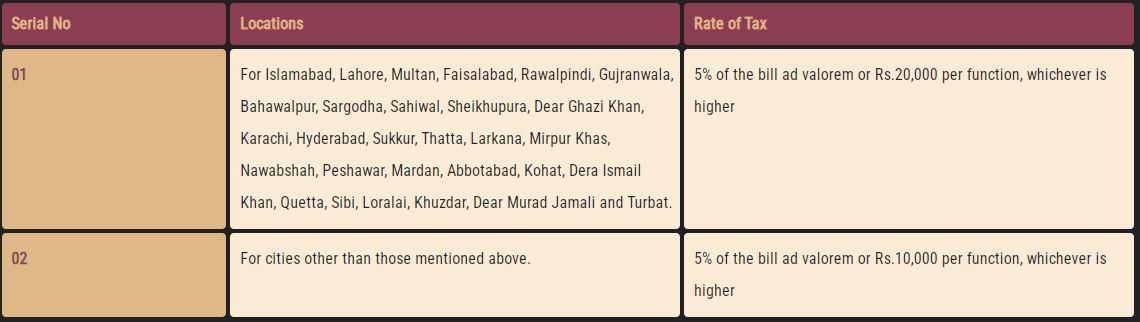

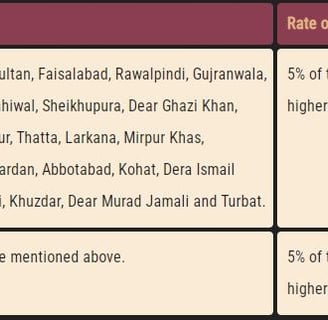

ADVANCE TAX ON FUNCTIONS AND GATHERINGS

Table: Advance Tax on Functions and Gatherings

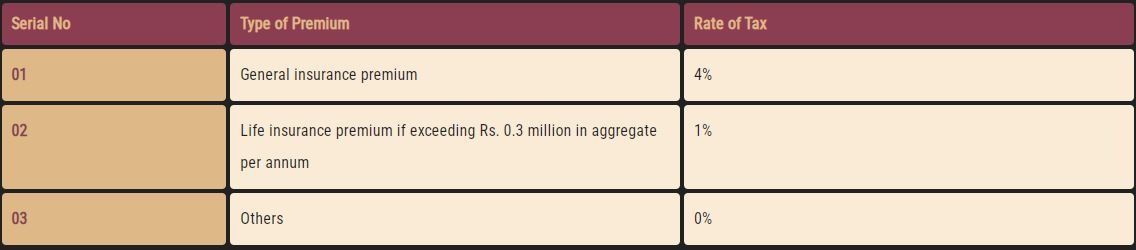

ADVANCE TAX ON INSURANCE PREMIUM

Table: Advance Tax on Insurance Premium

ADVANCE TAX ON EXTRACTION OF MINERALS

OUR CORE COMPETENCIES

COLLABORATIVE SKILLSET

Collaborative lawyers trust the wisdom of the group; lone wolves and isolationists do not do any good anymore.

EMOTIONAL INTELLIGENCE

Distant, detached lawyers are relics of the 20th century, the market no longer wants a lawyer who is only half a person.

TECHNOLOGICAL AFFINITY

If you can not effectively and efficiently use e-communications, and mobile tech, you might as well just stay home.

TIME MANAGEMENT

Virtually a substantial part of lawyers difficulties in this regard lie with their inability to prioritise their time.

About

Umeed Law Associates (LLB). Started in 2018 to provide legal services and also launched its website www.umeedlaw.com at Rawalpindi to fulfill the growing needs of the people searching the internet for immediate and easy access to understandable legal advise.

Adderss

2nd floor Umeed Law Chamber # 11 Zamrud khan block Kachehri, Rawalpindi.

Mobile: 03459468699

= 03189468699

Email: advmrizwanawan@gmail.com

© 2024. All rights reserved.